Story

September 25, 2025

September 25, 2025

Deaths Spotlight Dark Side of Europe-Backed Microloans in Cambodia

Country:

How the microfinance industry can paper over debt-linked suicides in Cambodia.

Om dit rapport in het Nederlands te lezen, klik hier.

Content warning: This article discusses suicide.

In a country that is struggling with poverty and high illiteracy rates, Europe-funded firms are handing out microloans with such high interest rates and fees people often cannot pay back their debt — and some of them see no other way out of their situation than by ending their lives.

First came a bad harvest. Then came the creditor. Now, Bun Ou is dead.

The cassava and pig farmer had been living in one of Cambodia’s most remote regions, Preah Vihear province, in the north of the southeast Asian country. When her farm became unproductive, loans seemed like a good way to stay afloat in between harvests.

She went to one of Cambodia’s biggest banks, Hattha Bank, and took out two microloans in 2022 totalling some 9,000 euros.

About a year later, the 51-year old was struggling to pay back the high interest payments, and the credit officer was breathing down her neck.

As a nonprofit journalism organization, we depend on your support to fund more than 170 reporting projects every year on critical global and local issues. Donate any amount today to become a Pulitzer Center Champion and receive exclusive benefits!

It came to a head one evening in January 2024, when a Hattha Bank credit officer came to Ou’s home to deliver a letter, asking her to show up at the bank two days later.

“In the event that you do not arrive by the above deadline, Hattha Bank will take legal action,” the letter read.

“My mother’s death has had a huge impact on the family.”

Kuon Suon

Ou, who could not read, listened to her daughter explain the letter. The next morning, she was found dead. A police report, seen by Follow the Money, ruled her death a suicide.

“My mother’s death has had a huge impact on the family,” her daughter Kuon Suon told Follow the Money. “Since she passed away, the house has been quiet, with all her children out working.”

The credit officer declined to comment. Hattha Bank did not respond to a request for comment.

This is not an isolated incident: Follow the Money reviewed family testimony, death certificates, police reports, and loan documents regarding suicides and attempts in five cases where debt-related stress or harassment were alleged to be factors.

The media and civil society have been calling out abusive practices in the country’s microloan sector for years. Yet, European governments and institutions continue to support the industry, buying into and selling a system that relies on questionable certification, an investigation by Follow the Money shows.

In the last 20 years, European governments — including through Dutch development bank FMO, France’s AFD, Belgium’s BIO, Austria’s OeEB, and Norway’s Norfund — have invested hundreds of millions of dollars into Cambodian loan firms.

Dutch development bank FMO has invested over 100 million dollars in Amret, 15 million dollars in LOLC, 5 million dollars in Chamroeun Microfinance, 51.5 million dollars in Sathapana, and 22.5 million dollars in Prasac. Finnfund 26 million dollars in Sathapana. Swedfund 15 million dollars in Prasac. France's AFD/Proparco 80 million dollars in Sathapana [LINK 8]. Norfund 85.3 million NOK, about 8 million dollars, in LOLC. Germany's DEG, subsidiary of KfW, invested 5 million dollars in PRASAC. FMO is 51 per cent owned by the Dutch government. Finnfund is 96 per cent owned by the Finnish government. Swedfund is fully owned by the Swedish government. AFD is fully owned by the French government (a state development agency) and Proparco is 85 per cent owned by the French government. Norfund is fully owned by the Norwegian government. KfW is 80 per cent owned by the German federal government and 20 per cent owned by the German federal states.

Four of those lenders have maintained the highest level of client protection certification — under a framework from the nonprofit group Cerise+SPTF — while continuing to engage in alleged abusive practices.

Borrowers and family members say pressures from credit officers have contributed to suicides. European agencies using these certifications as a factor when choosing investments are endorsing a system that can obscure borrower harm, while continuing to make profits and call these investments ethical.

“Microfinance institutions and their investors must take the situation seriously and ensure that their activities do not deepen the burdens faced by affected communities,” said Eang Vuthy, executive director of the Cambodian NGO Equitable Cambodia.

Certifying trust

Initially lauded as a way to empower the Global South’s impoverished population by handing out enough credit to start a small business or get it back on track, microloans have come under increasing scrutiny in recent years.

Critics of the worldwide industry say the practice has fueled over-indebtedness and failed to reduce poverty rates.

As early as 2010, for example, the BBC uncovered debt-linked suicides in India. Cambodia has been plagued by reports of abuses toward borrowers from civil society, local and international press. The country holds the record for the highest microfinance debt-per-capita in the world.

People are often trapped in their loans because of high interest rates of up to 18 per cent, the legal maximum, plus extra fees. Many Cambodians end up taking on additional loans from other firms or private lenders to make payments once they fall behind.

In a country of some 17 million people, Cambodian households currently hold 3 million microloans that are worth more than 15 billion euros, according to a new report by Human Rights Watch published on Thursday. The average loan is worth more than four times the median per capita income.

Cambodia’s Indigenous communities are among the most vulnerable. Many are not fluent in Khmer, the national language, and illiterate, with limited financial literacy, making it difficult to understand the terms of their loans.

Predatory microfinance lending has resulted in forced land sales, food insecurity, child labour, and suicides in Indigenous communities, Human Rights Watch found when interviewing over 50 Indigenous residents.

To incentivise better treatment of borrowers and formally rate lenders for their client protection policies, a certification programme was developed.

The nonprofit group Cerise+SPTF took over the certification framework from Smart Campaign in 2021.

The Smart Campaign also faced criticism over conflicts of interest. Mexican microfinance firm Compartamos Banco was Smart Campaign Certified in 2014. One of its shareholders was the D.C.-headquartered nonprofit Accion, which owned the Smart Campaign. https://www.theguardian.com/global-development-professionals-network/2014/oct/08/developing-countries-informal-economies-microfinance-financial-inclusion.

"We are deeply concerned by reports of deaths related to microfinance indebtedness in Cambodia."

International Finance Corporation

Much of Cerise+SPTF’s funding comes from European development agencies — some of the same institutions that are heavily invested in Cambodia’s microfinance sector.

Until recently, Cerise+SPTF evaluated and monitored rating agencies giving out the certifications. The rating agencies would apply Cerise+SPTF standards, judging if loan firms set responsible interest rates and fees, enforce respectful treatment of borrowers, and have a mechanism to resolve complaints from borrowers.

Cerise+SPTF is a joint venture between SPTF | US, SPTF | Europe, and Cerise. Cerise+SPTF pursues a common strategic plan and shares resources under a Memorandum of Understanding. Cerise is a French nonprofit.

Rating agencies like MFR and M-CRIL began certifying lenders globally, handing out gold and silver ratings to Cambodian loan firms such as LOLC Cambodia, AMK, Amret, and Sathapana Bank. Cerise+SPTF then displayed those ratings on its website.

A profitable industry

Hattha Bank, the institution that farmer Ou borrowed money from, is not currently certified — its certification from Cerise+SPTF’s predecessor the Smart Campaign lapsed a few years ago.

Still, it has benefited from the certification system: it still had its certification when Switzerland’s SIFEM provided it a 15-million-dollar loan in 2019. Norwegian Norfund loaned Hattha Bank 20 million dollars in 2021. Between 2015 and 2022, the International Finance Corporation approved investments of at least 125 million dollars.

Hattha Bank was still listed on the Cerise+SPTF website as having completed steps for client protection in September 2025.

Cerise+SPTF only marked the bank as “inactive” on its list of firms committed to client protection after Follow the Money sent questions about Hattha seemingly no longer meeting the requirements since October 2024. According to Cerise+SPTF's website, a lender will be marked as "inactive" on the list of committed institutions if it does not update its client protection assessment after two years. Hattha Bank's last listed assessment date was 1 October 2022. In emails provided to FTM, Cerise+SPTF notified Hattha Bank in May 2025 that "your organization will be removed from our website in the coming month if we do not receive any documents". Still, Cerise+SPTF never removed Hattha Bank from its website, only changing its "active" designation on 17 September 2025 following FTM's inquiry.

“While the events have shocked the community ... our investigation has confirmed that there was no debt pressure from AMK.”

AMK

European institutions have also heavily invested in other certified banks listed on the Cerise+SPTF website.

For example, European development agencies gave Cambodian bank Sathapana financing and loans in the last 10 years, including 51.5 million dollars from FMO, 15 million dollars from OeEB, 26 million dollars from Finnfund, and 80 million dollars from France’s AFD and Proparco. In March 2025, Sathapana’s certification was renewed for another three years, and the lender’s rating improved from silver to gold.

But that doesn’t mean that things are looking up for clients of Sathapana.

Over in Ratanakiri province in Cambodia’s northeast, an Indigenous Sathapana borrower also struggled to repay his debt. The person, who requested anonymity, said a credit officer told him to take out private loans — which have even higher interest rates — to repay around 850 euros in existing debt. The borrower said the credit officer even contacted local authorities about his overdue payments. Scared that he would face legal action and potentially go to prison, his mother attempted suicide in 2023, his family told Follow the Money.

Interest rates from informal lenders are often higher than those from microfinance firms or banks. They can range from 2 per cent to 30 per cent per month, compared to 1.5 per cent per month for a formal loan, according to a 2023 report from the Cambodian NGO Licadho.

Sathapana Bank did not respond to a request for comment.

Non-payment of loans is not criminalised in Cambodia, but credit officers regularly threaten borrowers with legal action, or to report them to police, courts, or government authorities. https://www.hrw.org/node/392118

That same year, an Indigenous AMK borrower in the same province died by suicide. His wife and daughter, who requested anonymity, told Follow the Money that he took his life because he did not have money to pay off his loan, and he was afraid of potential threats from the credit officer or legal action from AMK.

AMK said its staff had never put pressure on the man regarding debt collection.

"They say they are good to their customers, but for me, I experienced threats and they told me to sell my daughter."

Sal Thoeun

“While the events have shocked the community and the circumstances are complex, and we at AMK are deeply saddened by this case, our investigation has confirmed that there was no debt pressure from AMK or our client officers,” the firm said.

Also in 2023, Belgium’s BIO pledged a 15-million-dollar loan to AMK, highlighting AMK’s gold level rating in the press announcement.

“We take new allegations very seriously and are in contact with AMK to clarify the situation and explore how they can be thoroughly investigated,” BIO told FTM.

AMK’s gold level client protection certification does not expire until July 2026. M-CRIL, the rating agency that granted the certification, said in an email that the certification is currently “on hold”, but there is no indication of this on AMK’s listing on the Cerise+SPTF website or on AMK’s website.

Frances Sinha, a former AMK board member and current member of AMK’s social performance advisory committee, is also the director of M-CRIL, the ratings agency that granted AMK its certification. AMK stated that Frances Sinha was not involved in the certification process. “There is a clear and strong message to the M-CRIL assessment team that Frances’ association with AMK has no bearing on any findings,” M-CRIL said in a statement. Belgium’s BIO, which has current investments in AMK, said it “does not have reasons to believe she was involved, directly or indirectly, in the process where AMK sought proposals and selected an external rating agency”.

BIO has requested that AMK uphold its gold level certification “as a way to prove continuous implementation of the standards” in the specific context of Cambodia “where the risk of abuses of consumers’ rights is higher”.

BIO added that it requested an investigation of allegations of suicide cases of two AMK clients documented in The Guardian in 2023. Following the investigation, “BIO concluded that there were no elements indicating a direct responsibility of AMK’s loan officers in the suicide of those 2 persons.” “BIO's investment decision in AMK was guided by the institution specific outreach and proven track record in reaching underserved and vulnerable client segments, coupled with their longstanding and tangible commitment to responsible lending practices and client protection,” it said in a statement to FTM. BIO added that it has a grievance mechanism where individuals affected by its project can voice their concerns. “So far, we have not received any complaints related to these issues.”

M-CRIL, which had also certified Sathapana and Amret, said that “even a handful of such cases (out of several thousand clients) should not happen”.

Frances Sinha, M-CRIL’s director, added that one of the main “lessons” she has drawn from reviewing these cases in recent years is “that journalists — indeed any outsiders — have to be very careful when conducting interviews (particularly if in translation) and drawing inferences from short meetings/visits”.

In a similar vein, the firm Amret holds a gold level certification – but is still alleged to have engaged in abusive lending practices.

In February 2024, a credit officer from the firm Amret told Rochom Katael to sell her 14-year-old daughter to a venue commonly known for sex work to repay the family’s overdue loan payment of about 100 euros, according to Katael and her daughter who were both present when the credit officer came by.

Her mother, Rochom Tam, told her family she would rather die than lose their home because of the loans. The next month, she died by suicide.

Katael’s husband Sal Thoeun could not square Amret’s gold level certification with his own family’s experience.

“If it has good [client protections], then why do [the Amret credit officers] speak angrily and insult me,” he said. “They say they are good to their customers, but for me, I experienced threats and they told me to sell my daughter.”

In a statement, Amret said it “is very concerned about the disturbing allegations that you claim to have found concerning one of our clients”. The firm added that Amret had launched an investigation and would take action against the staff involved if the allegations were confirmed.

In May 2025, Amret received another gold level certification from the Milan-headquartered ratings agency MFR, which publicly praised Amret’s compliance with client protection standards “under the Cerise+SPTF methodology”.

MFR did not respond to a request for comment.

The Netherlands’ FMO has invested over 100 million dollars in Amret since 2013. In January 2025, when Amret was valued at approximately 550 million dollars, the development agency sold off half of the 20-per-cent equity stake it owned. Also in January, the investment company Advans, largely owned by the IFC and development agencies from France, the U.K., the Netherlands, Germany, and the European Union, benefited when it sold off its 56 per cent ownership of Amret. The IFC sold 10 per cent equity in the company in the acquisition.

“We are deeply concerned by reports of deaths related to microfinance indebtedness in Cambodia. We take such matters very seriously,” the IFC said. “IFC requires its clients to meet rigorous Client Protection and Responsible Finance Principles, which reflect good international practices in this space.”

Projects with direct and indirect investments in Cambodian microfinance lenders from some of the world’s and Europe’s biggest development funds amount to more than 1 billion dollars in funding.

This comes from the World Bank’s IFC, the Netherland’s FMO, France’s AFD, Norway’s Norfund, Finland’s Finnfund, Belgium’s BIO, the U.K.’s BII, Austria’s OeEB, Germany’s KfW/DEG/BMZ, Luxembourg’s LMDF and Switzerland’s SIFEM.

Updating the system

Amid rising criticism, from 2023 reports of Cambodian suicides in the Guardian to international investigations of abuses, rating agencies M-CRIL and MFR put four Cambodian loan firms – LOLC, Amret, AMK and Sathapana – under review. They did so at the request of Cerise+SPTF.

“We believed that the allegations raised in the Guardian were sufficiently serious, specific, and detailed to warrant the unprecedented request,” SPTF’s Executive Director Laura Foose said.

A litany of complaints: The International Finance Corporation’s watchdog in August 2023 began investigating alleged harms to borrowers by Cambodian lenders, including four with certifications: ACLEDA, Amret, LOLC and Sathapana. The harms included coerced land sales, threats from credit officers, and children being removed from school in order to earn money, according to a complaint filed by Cambodian NGOs LICADHO and Equitable Cambodia. And in September 2023, a Dutch government watchdog accepted a complaint from the same NGOs alleging abuses by Cambodian microlenders that received funding from Dutch social investor Oikocredit. Two of the lenders, Amret and LOLC, were certified.

Two years on, however, all four firms have maintained or renewed their certifications.

This means that a European funder looking on the banks’ websites, or Cerise+SPTF’s website, will still see the four institutions as having the highest rating in client protections.

Nitin Madan, director of the Responsible Inclusive Finance Facility for Southeast Asia at Cerise+SPTF, said internal discussions prompted the organisation to “step away from certifications”.

Cerise+SPTF also quietly made some changes to its system.

Under its new approach, implemented March 2024, Cerise+SPTF no longer promotes the certifications or labels specific rating agencies as qualified. Instead, the organisation now permits any organisation to award a certification under the Cerise+SPTF-developed framework: this means there is currently no oversight for the organisations giving out certifications, with no monitoring of their methodologies, conflicts of interests or auditor qualifications.

Cerise+SPTF never made a public announcement that it was amending the certification program. Impact investors such as Verdant Capital, Gojo & Company and FINCA continued to advertise incorrect information about the program as of September 2025. Verdant Capital and FINCA only removed the incorrect information after an inquiry from FTM. In a September 2025 statement, Belgium's BIO said its officers "do not recall having received the information on the change in certification process directly from Cerise+SPTF". A September 2025 email from Finland's FinnFund contained incorrect information which indicated it does not understand the changes made to the program. It claimed that Finnfund requires microfinance firms it invests in to receive a gold level certification from "an accredited auditor approved by Cerise+SPTF", despite Cerise+SPTF ending accreditation of rating firms in March 2024.

In a September 2024 email, SPTF executive director Laura Foose said that the 2023 events in Cambodia "prompted a wholesale reconsideration on Cerise+SPTF's part about the way we approach client protection certifications," ultimately leading to the decision to no longer designate rating agencies as qualified. In contrast, when contacted in September 2025, Luxembourg Aid & Development, one of Cerise+SPTF's core funders, claimed that the decision to no longer accredit rating agencies "was taken independently of the tragic events that unfolded in Cambodia." The Swiss Agency for Development and Cooperation, another core funder, also said in a September 2025 email "to our knowledge, this decision was not connected to the dramatic situation in Cambodia."

Cerise+SPTF still claims on its website that certifications are conducted by "qualified experts."

Despite these changes, the organisation continues to tout the certification programme as the “most rigorous” form of validation. It also still lists the firms with certifications on its website, and its name still appears on certificates.

Still, the organisation denied accountability for any alleged harms caused by certified lenders or investment decisions made based on certifications.

Before the recent changes, Cerise+SPTF publicly advertised the certifications as providing “an independent and objective opinion” [LINK 1] on a financial institution’s client protection practices, and claimed that its approved rating agencies had “robust systems to ensure impartial decision-making.”

“Cerise+SPTF develops and promotes voluntary standards to guide responsible practice in the market. We do not certify lenders, nor do we take accountability for individual institutions’ actions,” it said in a statement.

“Our role is not to be placed under suspicion but to be acknowledged and supported as a driver of responsible inclusive finance and consumer protection practices,” executive director Foose said.

Development finance researcher Milford Bateman, however, rejected that argument. In his view, the certifications helped government development agencies reap profits from investments in microfinance firms while advertising them as a form of corporate social responsibility.

“They use [the certifications] to actually wash their social impact investments, which are actually making a shedload of money,” he said.

According to him, investors can say: “We're helping Africa and Asia get back on their feet. We're putting all that money in, and these guys say how good we're doing. We're only supporting gold standard microfinance institutions.”

Taking matters into their own hands

But while Cerise+SPTF is distancing itself from the certifications on paper, borrowers from these firms are still struggling on the ground.

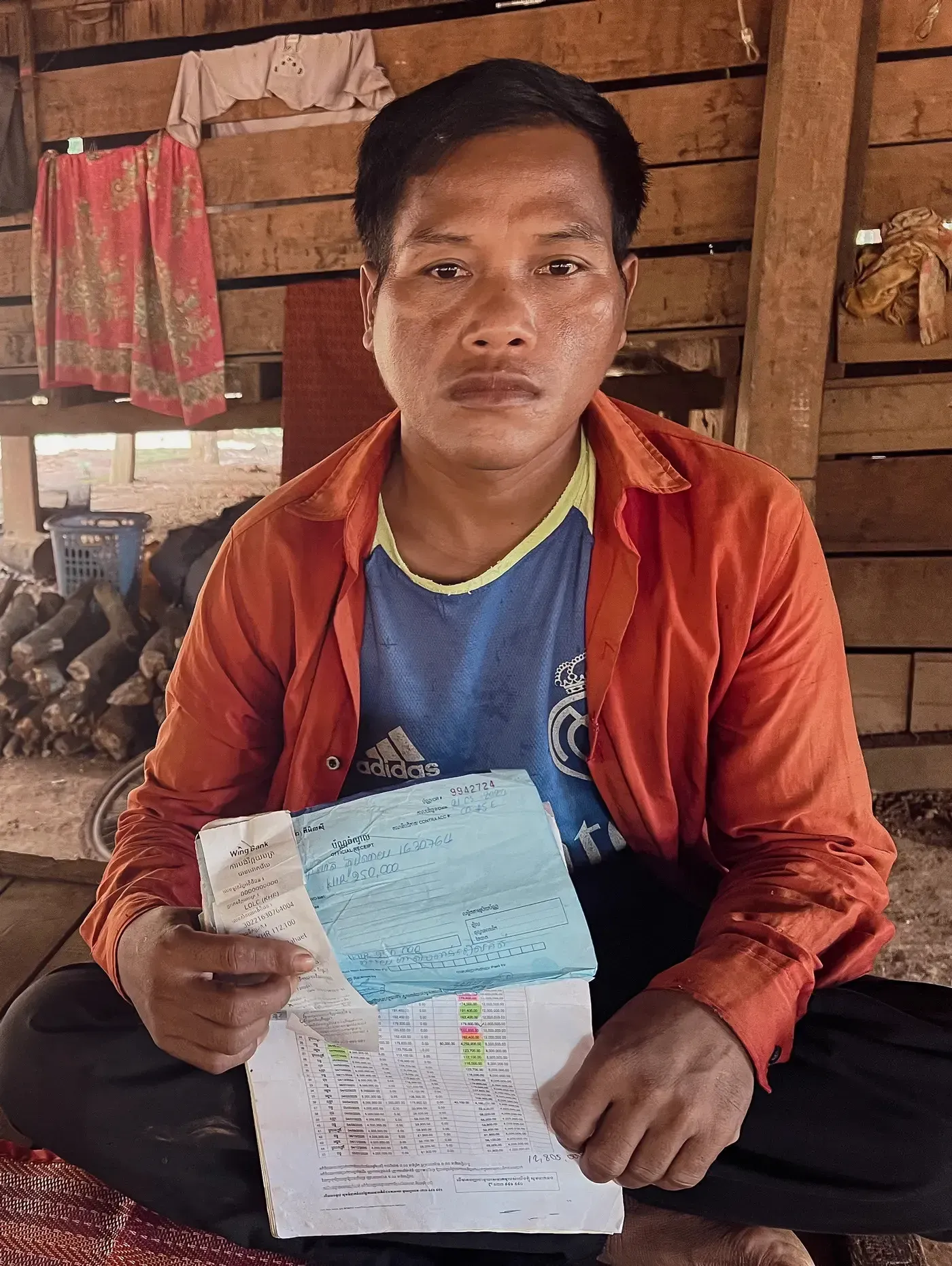

Just last year, the same year that Ou died and within a month of Cerise+SPTF switching its approach, 41-year-old Romam Pahaet encountered the same difficulties.

Like Ou, the Indigenous man had seen his crops fail. The cassava crop had yielded little harvest on his farm in northeast Cambodia, and he was running out of money. His sister had already sold off a piece of land to help him pay back a 4,000-dollar loan he had taken out from the firm LOLC, which has received funding from Dutch development bank FMO and Norway’s Norfund.

It still wasn’t enough.

The credit officer was showing up at his house almost every day.

In a good year, Pahaet could expect to earn about 1,600 dollars – but he would have to pay almost that entire amount to the loan firm: 1,300 dollars in payments and interest, according to his credit statement.

While Ou didn’t live to tell her story, Pahaet did.

“I was so stressed and angry after hearing the credit officer insist on forcing me to sell my land, my home, my motorbike and take out private loans,” Pahaet said. “That is why I tried to kill myself.”

Pahaet survived. A few weeks later, in April, he attempted suicide a second time. To the relief of his family and friends, he lived.

The credit officer could not be reached for comment.

Pahaet decided to take matters into his own hands and filed a complaint with LOLC, hoping to have his loan forgiven because he was destitute and mentally unwell. Around the same time, LOLC was able to maintain its gold level certification following a review by the ratings agency MFR, according to the loan firm.

LOLC agreed to meet with him, and restructured the loan with a lower monthly interest payment in May of this year.

“Our Code of Conduct strictly prohibits coercive collection practices, including pressuring clients to sell land or to borrow from informal moneylenders,” LOLC said in a statement, adding that the case had been reviewed. “We worked with the borrower to restructure their loan with the aim of reducing financial pressure.”

But Pahaet, who is illiterate and not fluent in the national language, said he did not understand the terms of the new contract.

“Cerise+SPTF is desperately trying to keep the thing going. Because, otherwise, what do they do?”

Researcher Milford Bateman

The new monthly interest payment, about 19 euros, is still too much for him to afford: he currently earns less than 70 euros a month, he said. He has already missed payments and the family is eating less to keep their spending down.

The practices of the lender haven’t changed either, he said.

“I’m still nervous, not knowing when or what the bank will do to me since I gave my thumbprint on the new loan document,” he said. “The credit officer is constantly calling me to ask me to pay the interest payment but I am unable to pay.”

Researcher Bateman said the documented abuses in Cambodia have discredited the certifications, and argued that Cerise+SPTF carries responsibility for propping up the industry.

“Cerise+SPTF is desperately trying to keep the thing going. Because, otherwise, what do they do?”

For now, stories like that of Ou continue happening in Cambodia.

Three days after her funeral, a Hattha credit officer came to the family home again to demand payment, according to Ou’s family.

“Don’t threaten people with going to [authorities] if they don’t have the money,” Ou’s daughter Koun Duong said. “Don't extort money to your heart’s content.”

Reactions

The Dutch Entrepreneurial Development Bank FMO said in a statement that, in response to issues in the Cambodian microfinance sector, it “has taken a more cautious approach and stopped providing support to Cambodian microfinance institutions (MFIs) that pursued aggressive growth strategies”.

While FMO highlights certifications in its impact reports and lists them as part of the rationale for investments, FMO told FTM that “the fact that an institution is client protection certified does not serve as sufficient evidence to proceed with a transaction”.

Norfund said that it “takes the reported cases of suicide and attempted suicide among borrowers and their families extremely seriously,” the development finance institution said in a statement. “We evaluate client protection measures independently of certifications during our due diligence and remain committed to rigorous client protection assessments.”

France’s AFD Group said that “in Cambodia, in a spirit of prudence and responsibility, AFD Group has reassessed its strategy in this sector since 2022”. It added that it has not signed new Cambodian microfinance financing agreements since 2022. “To date, there remains residual exposure to Sathapana (EUR 29 million) and LOLC (EUR 5.7 million) institutions, with which AFD Group still has contractual commitments.”

It added that it has donated EUR 5.56 million to Cerise+SPTF in total.

“AFD Group continues to support certifications and to work with skilled and experienced rating agencies that follow the highest international standards. This requirement is at the very core of our approach,” it said.

Finland’s Finnfund said in a statement: “The information regarding additional suicide cases is deeply concerning, and we take such claims with the utmost seriousness … Client protection certification remains as one of the practical and strategic monitoring practices.”

In Austria, OeEB said that “we carefully select the partners we work with and carry out thorough environmental, social and human rights due diligence with a special focus on the implications for end borrowers before providing loans or equity capital”.

“Microfinance institutions financed by OeEB are contractually required to adhere to internationally recognized Client Protection Standards,” it said in a statement.

A spokesperson for Switzerland’s Federal Department of Foreign Affairs said “the Swiss Investment Fund for Emerging Markets (SIFEM), which also upholds the Cerise+SPTF’s client protection standards, no longer has any financial exposure in Cambodia after the repayments of the loans granted to Hattha and Amret in 2024”.

After publication of the article, Amret said its investigation of the case involving its client had shown no evidence of the allegations. “The official complaint by the customer was fully resolved to the customer’s satisfaction,” the company's spokesperson said.

Eung Sea contributed reporting.

If you are struggling, you are not alone. In Europe, you can find international hotlines at https://findahelpline.com, or if you’re elsewhere, please look up local resources available in your country.

In the United States, call or text 988 or chat 988lifeline.org.