The Pulitzer Center and the College of William & Mary continue their unique initiative to provide...

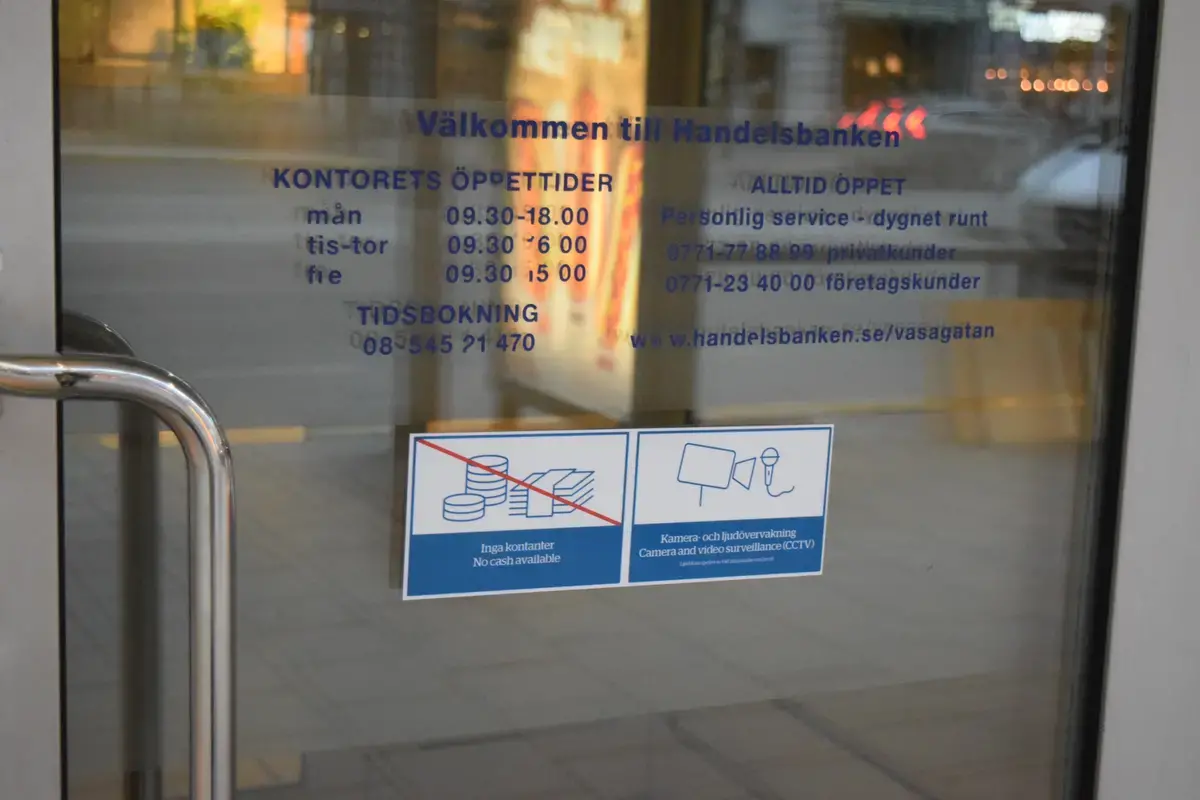

On the front door of a bank only a block away from Stockholm's Centralstation is a sign that reads "Inga kontanter" with an English translation below: No cash available. Walk a few more blocks under the gray winter sky, and see signs hanging on the front doors of coffee shops that say "Endast kreditkort" or "Vi är en kontanantfri coffee shop" — "only credit cards" and "we are a cash-free coffee shop," respectively. Amble through the gift shops of the ABBA Museum or Fotograsfika, a popular contemporary photography center, and signs near the register alert customers that they, too, do not accept cash.

Less than 400 years after it became the first European country to introduce banknotes, Sweden is on track to become the world's first cashless economy.

And while proponents of this no-bill world believe it will lead to a reduction in crime and save the government money, others are worried. Defenders of rural areas, small businesses, and pensioners say that some people are being left behind, while other critics worry about the potential security risks.

Data from the Riksbank, Sweden's central bank, also suggests that anger toward the decline in cash has increased. In 2016, 31 percent of survey respondents expressed negativity toward the decline, compared to 24 percent in 2014. The increase in negativity does not mean that respondents lack access to alternative means of payment; 97 percent of respondents in 2016 said that they had access to a bank card.

"It's not a problem for me," said Jan Andersson, chairman of PRO Skåne, the southernmost branch of Sweden's largest pensioners organization. "I have cards. I also use Swish. And I have Internet to pay my bills and so on. But a lot of people who are 75, 80 years old–we live longer and longer–especially among them, they are left behind."

James McAndrews, an economist and fellow at the Wharton Financial Institutions Center and former director of research at the Federal Reserve Bank of New York, says that Sweden is an example of an ideal society to attempt a cash-free economy because of the relative homogeneity of both its population and payment instruments. Higher rates of internal migration and immigration are linked to greater use of cash; more ways to pay, from Venmo and PayPal to American Express and Visa gift cards, mean coordinating an approach to purely electronic payment to replace cash becomes nearly impossible.

"I think that the United States is quite a long way from the Swedish-level of electronification of payment systems," McAndrews said.

But Björn Eriksson, former president of Interpol, the international police association, and one of the most visible opponents of a cash-free Sweden, hopes that Sweden never gets to a banknote-free economy.

"I don't want to have a society where some people can't participate at all because they're old-fashioned or if they don't have the skill or whatever it is," he said.

Sweden's acceleration toward a cashless society began in 2005, when the country's government delegated the power to decide cash and payment systems to a few major banks. In 2012, the Riksbank decided on the new design for some of its banknotes, the most that it has ever changed at one time; many Swedes opted to deposit their invalid bills rather than change out. In December of that same year, six major Swedish banks–now 10–collaborated on the mobile app Swish, a real-time payment system without fees for private customers. (The closest American equivalent to Swish would be Venmo, which charges a small fee for real time transfers or offers a waiting period without a fee.)

Eriksson began Kontantupproret (literal translation: Cash Uprising), a network of organizations bound together by an interest in keeping cash in the Swedish economy, in 2015. Included in the network are pensioners organizations, such as Pensionärernas Riksorganisation (PRO), and organizations that represent small business owners and rural areas.

"We can see that the banks don't want to discuss this, the politicians want to avoid to avoid the question," Eriksson said. "We want to have it on the political agenda.… the politicians underestimated in the beginning the public anger when a lot of people are left aside."

Building on the popular frustration with cashless banks, Andersson rustled up a local television news crew and some krona to make a point last year.

With the film crew recording his every move, Andersson walked into a local branch of his bank to make a deposit. But there was a problem: the branch did not accept cash. In fact, none of the branches in his city of roughly 140,000 people accepted cash. Instead, he had to travel to Malmö, a city with double the population roughly 40 miles away. Andersson couldn't even use his cash at the popular restaurant next door.

"And I asked the owner, 'Why? Why can't I?' And it's because of the bank. 'If I get notes and coins from you, then what can I do with them?'" he said.

As evidenced by Andersson's anecdote, few bank branches in Sweden accept cash deposits anymore. And just as depositing cash becomes more difficult, so does withdrawing it. The increase in coffee shop signs advertising a no cash policy means that the sight of graffitied, robin's egg blue ATMs becomes rarer. Every month, banks rip out ATMs, removing more than 550 between 2012 and 2016, according to data from Riksbank.

The country's central bank, the Riksbank, predicts that the country will be considered a cashless society by 2030, and an October 2015 study published by the KTH Royal Institute of Technology in Stockholm predicted that Sweden would be the first cashless society.

Both Andersson and Eriksson believe that Sweden's government should adopt a policy like that of Norway that requires every bank branch to accept bills and coins. Eriksson also proposed withdrawal fees as a way to incentivize banks to continue to circulate cash.

Both men, though, say they are not against the development of digital payments or their use.

"We have a lot of education within our organization to teach elderly people how to use the internet, how to use the apps or those modern things all around," Andersson said. "But there are fairly many elderly people who want to use notes and coins. They are used to it, and they don't want the other way. They don't have access to internet, they have no smart phones, they don't know the new systems ... We understand that there will be changes to society, but we can't leave a large group behind this development. We have to have both."

In addition to those who do not want to learn how to use new digital payments, Andersson points out that the elderly who suffer the most from the decline in cash tend to those who are older, "75, 80 years old," live further from urban areas, or lack internet access.

For example, Swish, while intuitive and accessible to the visually impaired, requires a smart phone and internet access for use. Although wifi is plentiful in Stockholm, travel farther north and it becomes scarcer. (Sweden's prime minister Stefan Löfven announced in 2017 a plan to get all of Sweden connected to the internet by 2025.)

Per Ekwall, a spokesman for Swish and proponent for a cash-free society, says that their research shows that social contact, not region or age, determines if one will become a Swish user. Ekwall credits the 50 percent penetration rate for Swish within the over-65 segment to children and grandchildren introducing the app to their elders.

"We can see, for example, that older people that are very active in organizations, like bowling, they tend to use Swish a lot because in that social context it's used," Ekwall said. "Then they don't think it's anything strange, and it doesn't have anything to do with age… although you're more active when you're younger."

Setting aside being able to conduct transactions without cash, a cash-free society presents other risks. From 2005 to 2015, the percentage of Swedes exposed to robbery dropped, according to a government survey. But credit card fraud has been rising rapidly.

Andersson has also had this experience. His bank notified him about unusual activity on his card before he even noticed the fraudulent transactions.

"I have been a victim of fraud," he said. "I don't know how, but in some way people used my card. My bank said that they had stopped the use of my card. I still don't know how they got the number of my card."

Banks will have to reckon with the rise in fraud and identity theft, creating what Eriksson calls a "transactional cost" to the benefits of a cash-free society for banks: fees, fees, and more fees for the banks' bottom lines.

Fraud is not only limited to small-scale personal encounters like Andersson's. McAndrews says the 2017 Equifax breach is an example of the dangers of electronic payment; with more confidential data available electronically, the more likely another large breach will occur, he says. Eriksson also noted a rising concern about hackers, such as those from Russia, who could render all of Sweden "helpless" simply by turning off their data system.

Privacy presents another risk for a cash-free society. Eriksson said that when he asks those who support a cash-free society if they still use cash, they usually refer to activities where they do not want to be identified, like when they go to the liquor store.

"You are being traced by Big Brother all the time," he said. "We can easily take the next step. When is the surveillance substituted with political action?"

McAndrews proposes another pessimistic macro-level hypothetical: negative interest rates. Although he believes that Sweden is better suited than the United States to remove bank notes from circulation eventually, McAndrews is more skeptical with regards to negative interest rates, another potential benefit floated by economists. If a bank charges negative interest rates — say, three percent — in an economy with cash, anyone looking to deposit a paycheck into their bank account would choose to hold onto dollar bills instead of losing money in their savings account. However, a cash-free society removes that choice, and the only available escape becomes spending that money.

"That's of course the objective of a central bank when it's attempting to combat a recession, so that could be very powerful monetary policy at a time, when currently, bound by a zero-percent interest rate, monetary policy can be ineffective in those times…" McAndrews said. "However, the unpopularity of [negative interest rates], and for various other technical reasons that I've written about, I don't think that we will ever get there."

Eriksson offered up a less technical reason for why all hope is not lost yet for those who oppose a cashless society. He believes that the upcoming general election in September 2018 could provide a means for citizens angered by the decline in cash to express their feelings and provoke less apathy from politicians. According to him, smaller political parties have reached out to Cash Uprising looking to strike up more votes.