Story

![]() February 2, 2023

February 2, 2023

Flood Insurance is a “Hot Mess.” That’s a Growing Problem for Hampton Roads Homeowners.

Country:

Why is it so hard to find an affordable place to live in Hampton Roads?

Karen Speights’ flood insurance bill for her home in Norfolk’s Chesterfield Heights has risen almost every year in the last decade.

“That’s been a burden,” 64-year-old Speights said.

It’s why she signed onto a pilot project with a local startup to see what might reduce her home’s flooding risk. It’s been going on for more than a year while she lives elsewhere.

As a nonprofit journalism organization, we depend on your support to fund critical stories in local U.S. newsrooms. Donate any amount today to become a Pulitzer Center Champion and receive exclusive benefits!

It was worth it, she said, so she could see big drops to her flood insurance premium.

“If I can’t get the flood insurance down, then I may have to leave,” Speights said last year. “It’s eating up a lot of savings.”

To her relief, that insurance bill is soon set to decrease.

But a recent overhaul to the National Flood Insurance Program may not mean the same for everyone who puts in the same work.

Hampton Roads officials say the changes have nearly eliminated financial incentives for homeowners to invest in flood mitigation work.

It’s one of many concerns about the changes.

About 71,000 Hampton Roads residents currently have flood insurance. Most of those are people who are required to, because they carry a federally backed mortgage in a certain geographic zone FEMA determines to be high-risk.

The recent changes could impact which homes are affordable and where, local officials said—all while the region faces a serious housing crisis.

“It’s a hot mess,” said Mary-Carson Stiff of the Norfolk nonprofit Wetlands Watch.

How we got here

Congress created the National Flood Insurance Program in 1968.

“At the time, flood was viewed as an uninsurable risk and coverage was virtually unavailable from private insurance markets,” according to the National Association of Insurance Commissioners.

The program hasn’t changed much since then. It covers more than 90% of mandatory flood insurance policies and it’s more than $20 billion in debt, after paying more in claims than it earns.

In 2021, the Federal Emergency Management Agency, which manages the program, started rolling out the first major overhaul in years, called Risk Rating 2.0.

Agency officials have two goals.

The first is to make premiums more equitable. Before the change, the owner of a 200,000-square-foot home would pay the same as the owner of a 10,000-square-foot one next door, for instance.

The new system accounts more fairly for a home’s value when determining rates. Stiff said that aspect seems to be working.

The other aim is to make the NFIP more solvent. In an email to WHRO, FEMA officials said that will happen over time by getting “a much clearer picture of flood risk.”

The government mandates flood insurance only for those who live in a Special Flood Hazard Area. You can see the outline of these areas on a rate map—originally named such because they determined a community’s insurance rate.

That goes out the window under Risk Rating 2.0. The maps still determine whether or not you must buy insurance—but not how much you’ll pay.

The new methodology is based instead on a mix of factors about each home, such as its distance to water and the amount of coverage requested.

“The primary factors are easily understood by most property owners,” FEMA officials told WHRO.

The algorithm is proprietary, so only FEMA and its private partners know how rates are calculated.

It’s unclear how many factors are included, or how each of them is weighted. It’s also subject to change each year.

That “black box algorithm” makes it virtually impossible for people to account for future costs, Stiff said.

A Threat to Affordability

Flood insurance has always been a big part of Barry Jenkins’ job.

The Virginia Beach Realtor started selling houses in Hampton Roads decades ago.

When flood insurance changes, it’s as big of a deal to owners and potential buyers as school redistricting.

“You think about all the impacts that that has on people that were potentially buying in a neighborhood or people that feel that they need to move,” Jenkins said.

“It's very similar with flood insurance. As the rates have gone up and down and left and right, it always causes a little bit of disruption.”

Selling homes in flood-prone areas can be tricky. Jenkins said his goal is always to make a buyer informed of the issue and they can choose how much risk to take on.

Risk Rating 2.0 makes that a little more difficult.

Prospective buyers can likely figure out what they’ll pay right after purchasing their home. In many cases, they can assume the policy of the former homeowner.

But how will flood insurance play out over the course of a 30-year mortgage?

That’s now much trickier to assess.

Yorktown Realtor Mike Reames said that information is even more important to buyers and owners given the current affordability crisis.

“The greatest benefit of homeownership is locking in a mortgage price so that you are predictable for 30 years in your housing costs,” Reames said. “That was one of the main reasons why the American Dream was to buy a house.”

Rising flood insurance costs in coastal communities complicate that.

He often has clients who are interested in a home, then find out the potential flood insurance.

“It can make (it) unsellable,” Reames said.

It happens particularly with lower-valued homes, he said. Those with the money to buy more expensive homes may not mind paying higher insurance premiums, while it could knock those barely able to buy a home out of the running.

Matt Simons, coastal resilience manager with the city of Norfolk, said everything affects the bottom line.

“Any dollar that cannot go towards their principal interest and has to be taken away from that, is just less home that they, at the end of the day, can afford.”

Older homes that were built before modern flood regulations are often more at risk, he added. Newer constructions already up to code may have lower insurance rates.

The cost of some policies may go up and make starter homes less affordable, Simons said.

“If we've allowed it to become so expensive that it’s an impediment, that's a risk,” he said. “We want to maintain […] opportunities to homeownership and new wealth creation.”

Rising Costs

Congress caps annual flood insurance rate increases at 18%. It will take as long as a decade for some homeowners to reach their full new rate.

By then, the calculations may have changed again.

“That’s the number we really want to know,” Simons said. “If a policy is set to increase—what I need to know is what the finish line is.”

Ben McFarlane, senior regional planner with the Hampton Roads Planning District Commission, told Norfolk City Council last year that it was previously rare to see increases as high as or beyond the 18% annual cap.

“We’re going to start seeing that more and more frequently,” he told them.

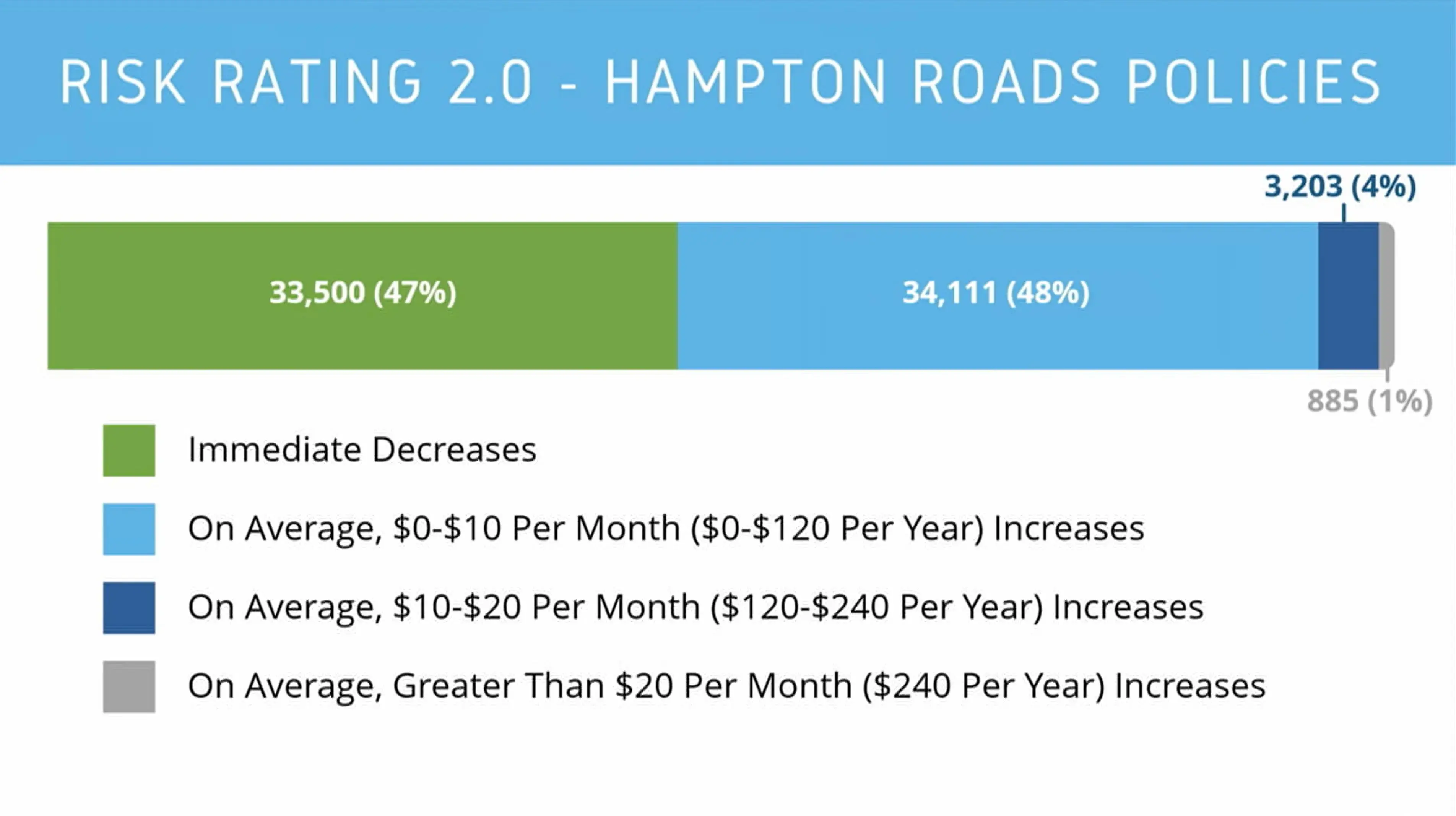

Hampton Roads was expected to see slightly more immediate increases in flood insurance premiums under Risk Rating 2.0 than decreases.

The Peninsula—particularly York and James City counties, Poquoson and Gloucester—saw the most increases.

About 10% of Hampton Roads residents with flood insurance also completely dropped their coverage over the past year, in line with national trends.

Norfolk Councilwoman Andria McClellan, who often encourages local homeowners to purchase flood insurance, tweeted last summer that the cost of her policy rose by more than 40%.

“I’m not surprised that folks are dropping their policies,” she wrote. “This is a BIG problem.”

Overall participation in the NFIP has fallen in the past year by as much as 20%, according to the Coalition for Sustainable Flood Insurance.

The group found that higher-income households are more likely to have flood insurance than lower-income households—even though incomes are lower in areas mandated to have insurance.

Not enough people in Hampton Roads have flood insurance to begin with, local officials say. Some assume homeowner’s policies pay for flood damage, but most do not.

The new system makes flood insurance less desirable for people who may voluntarily want it, Hampton Roads leaders worry.

When flood protection’s not enough

Mike Vernon is known locally as the “flood fixer.”

His company, Flood Insurance Hampton Roads, helps people make improvements that better protect their properties from flooding, therefore reducing their insurance premiums.

Risk Rating 2.0 no longer seems to reward that work, he said. He’s concerned his business and others in the flood mitigation industry will suffer as a result.

FEMA no longer places an outsized emphasis on a property’s elevation to determine premiums.

Vernon said he could previously guarantee clients their premiums would drop based on his work—which includes moving mechanical equipment to higher floors and adding basement flood vents—sometimes by thousands of dollars.

“Now they don’t care about any of that,” Vernon said.

That gives people less incentive to invest in the measures, he worries.

FEMA told WHRO that the old system often over-rewarded mitigation work.

“Premium reductions for mitigation activities should closely match the anticipated reductions in flood loss payouts,” officials wrote in an email.

They said the elevation of a structure’s lowest flood is still one of the most important factors determining a property’s premium.

Solutions

Hampton Roads officials are working on ways to adapt to the new system while also pushing FEMA to reveal more about how it operates.

Some local governments are already part of a program, called the Community Rating System, that provides discounts for residents whose leaders invest in flood management work.

Norfolk currently has the most advanced level under the program in Hampton Roads, providing the biggest discount to flood insurance holders in the city.

However, property owners can’t realize that advantage until they’ve reached their full new flood insurance rate, Simons said.

Officials want to see how the regional private insurance market can help. FEMA itself hopes to shift more policies to private insurers.

Norfolk nonprofit RISE Resilience Innovations dedicated its most recent funding challenge to working with the industry and cutting total premiums and payouts in half.

Despite its problems, the NFIP is still the most reliable option, said Stiff with Wetlands Watch. It’s the only one required by law to make payouts, even if it takes years.

“If a storm occurs and it's so great that it bankrupts the private flood insurance program or company, you are not going to get any sort of relief,” she said.

“A lot of people in this industry are very concerned about the false level of security that comes with some private flood insurance companies.”

Some private insurers already don’t want to serve risky coastal markets, like Florida.

Stiff said FEMA faces many challenges running the NFIP because it has to operate as a government agency and a business.

The new risk assessment system helps the agency with the latter.

Flood insurance remains people’s best tool to manage their risk, said McFarlane with the planning district commission.

But “FEMA’s making our job a little bit hard right now.”