Story

![]() January 31, 2024

January 31, 2024

Cambodia’s Indigenous Communities Renounce Communal Land Titles for Microloans

Country:

How development agendas and government policies undermine efforts by Indigenous communities to...

- Indigenous rural communities in northeastern Cambodia are struggling under debts that have ballooned from modest microloans with high interest rates.

- Microlending as a means of increasing communities’ access to finance is strongly supported by the World Bank, but runs counter to efforts to grant communal land ownership of homes, farmlands and sacred forests — another World Bank initiative.

- Entire villages have opted out of the communal land titling program because it would prevent them from using this land as collateral for microloans and selling land to outsiders, often to repay debt.

TA HEUY, Cambodia — Cambodian farmers Nuoy and Nangkek were both in their late 20s when they took out their first microloan in 2018 for around $600 to help grow their crops. Today, the couple owe more than $10,000 to two financial institutions charging 18% annual interest.

Like many borrowers in a country with one of the highest rates of microloans per capita, the couple spiraled deeper into debt as they borrowed more money to keep up with monthly payments on existing loans. They also resorted to borrowing from several neighborhood lenders who charged even higher interest.

Poor cashew harvests brought by heavy rains destroyed much of the only source of income the two had, forcing them last year to migrate to another part of the country to work in a car parts factory. The debt and stress have mounted.

As a nonprofit journalism organization, we depend on your support to fund journalism covering underreported issues around the world. Donate any amount today to become a Pulitzer Center Champion and receive exclusive benefits!

“I can’t sleep, I’m always thinking about the loan, can I get the money, how can I pay back the debt — now we are spending all our time trying to get money,” says Nuoy, who along with his wife requested a pseudonym to avoid repercussions from authorities and the microlenders.

Most of the couple’s microloans had been collateralized by farmland in their ethnic Kreung and Brao village of Ta Heuy in northeastern Ratanakiri province, one of the regions of Cambodia most heavily populated with Indigenous ethnic minority communities. To repay their debts, they now plan to sell most of their farmland.

Their debt crisis parallels and highlights a turning point in Ta Heuy village.

For nearly a decade, the Indigenous community had sought to gain legal ownership of its customary lands and sacred forests. Then, in June 2022, at the final stage of the arduous bureaucratic process, the vast majority of the village — Nuoy and Nangkek included — thumb-printed a petition to withdraw the application, shocking authorities and alarming Indigenous rights NGOs.

Microloans are the primary reason, community leaders and residents told Mongabay.

The special form of land ownership the village renounced is known as an Indigenous Communal Land Title (ICLT) and was designed to protect against the threat of land loss and deforestation. Under the ICLT, individual families would be barred from selling their land outside the community.

As envisioned by Indigenous rights activists, the communal land ownership promised a bulwark of protection for villagers’ livelihoods and cultural heritage. Besides encompassing homes and farmlands, the communal land title was also designed to protect villages’ spirit and cemetery forests, and set aside “reserve forest” for future generations.

The World Bank, a proponent of the ICLT, argues that empowering Indigenous peoples to protect their customary lands and maintain their traditional agricultural practices better safeguards forests and biodiversity.

But now another policy championed for decades by the World Bank — the $16 billion microfinance industry in Cambodia — had come into conflict with the entire ICLT framework.

Conflicting interests

The situation in Ta Heuy village mirrors a phenomenon emerging in Cambodia, in which some Indigenous communities, often frustrated by long-delayed ICLT applications, are rejecting communal ownership, largely to retain access to microloans.

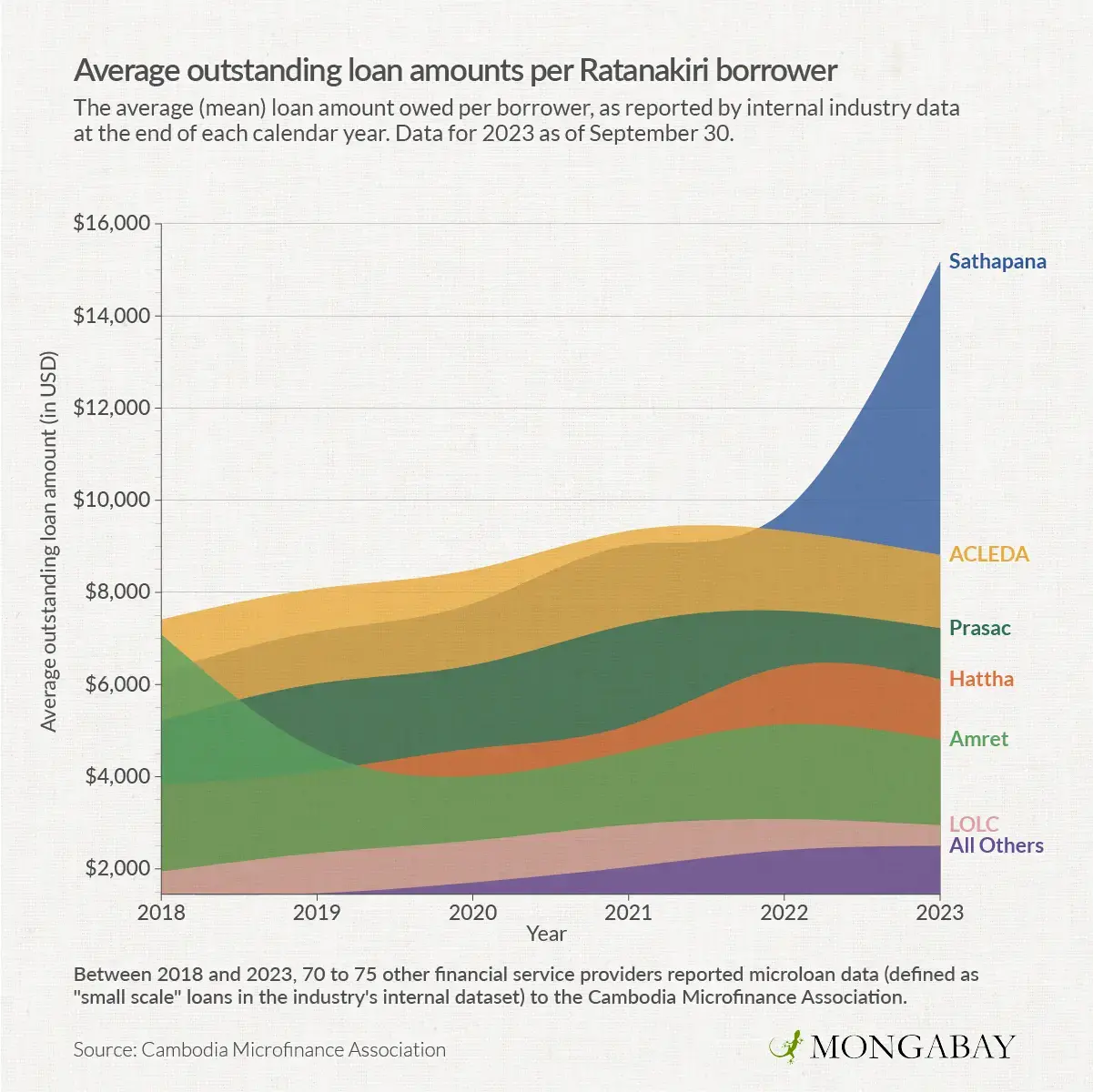

Dozens of registered microlending companies in Cambodia hawk loans typically collateralized with land titles, with the average borrower owing more than $5,000 in outstanding debt — an amount greater than most rural Cambodians’ annual incomes. But plots of land within an Indigenous communal land title, which includes individually owned farmland and homes, can’t be mortgaged or sold outside the community.

By the time their ICLT application was nearing approval, most Ta Heuy villagers had already spent years relying on microloans to fund farming, home-building and other needs. While some had improved their standards of living, others were so heavily in debt that they couldn’t afford to lose the ability to mortgage or sell their land, more than a dozen Ta Heuy villagers and community leaders told Mongabay.

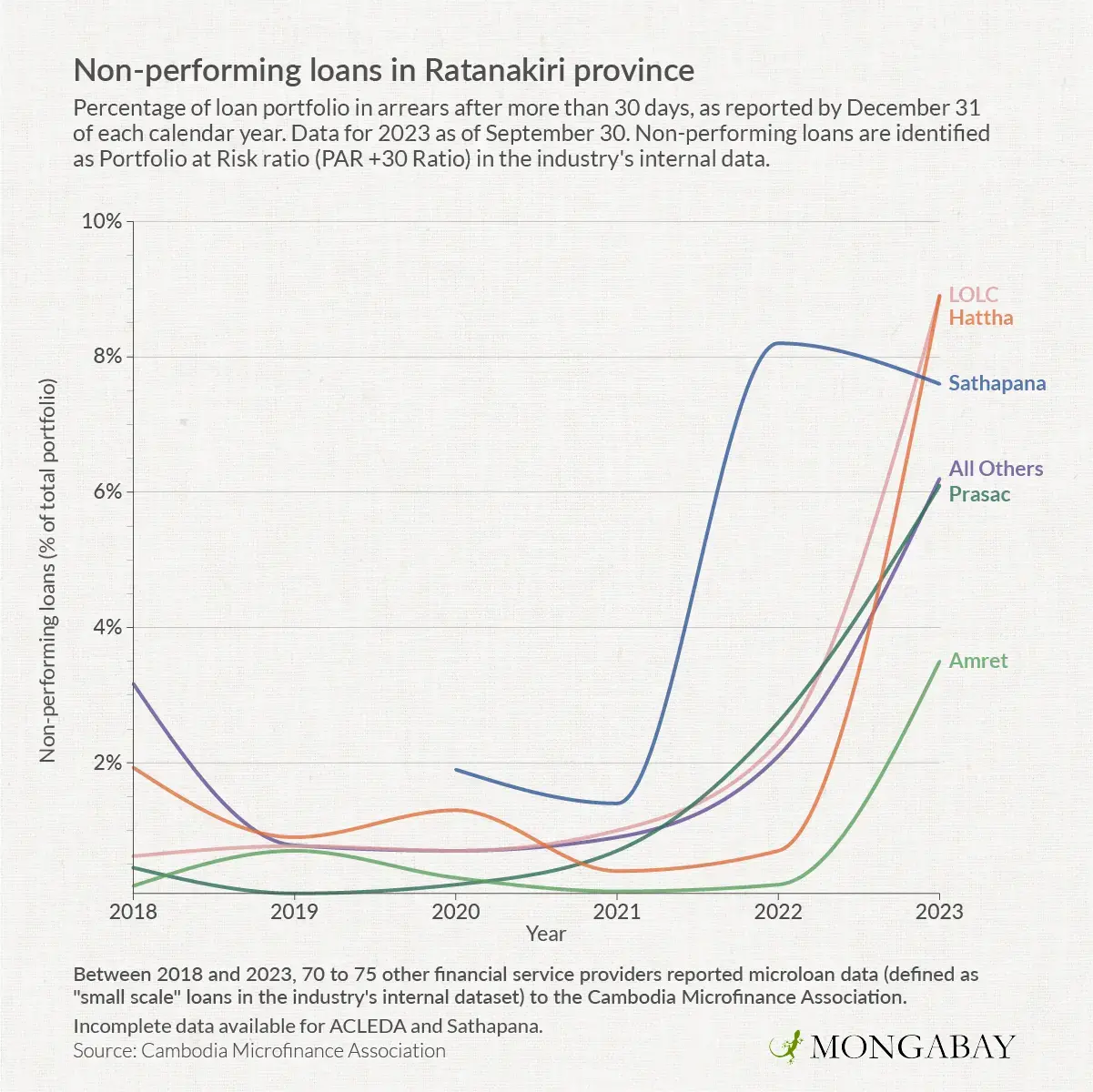

Internal industry data obtained by Mongabay show increasingly higher rates of nonperforming loans — measured by the percentage of a microlending institution’s portfolio in arrears after 30 days — reported by microlenders across Ratanakiri province.

In Koun Mom district, where Ta Heuy village is located, 11.6% of the loan portfolio held by LOLC Cambodia – one of the country’s biggest microlenders – was in arrears after 30 days as of September 2023. Nuoy and Nangkek were among the growing number of borrowers who had fallen behind on repayments.

The problem facing these villages appears in part to be the culmination of conflicting policies of the World Bank Group and other major development funders invested in both Cambodian Indigenous land rights and microloans.

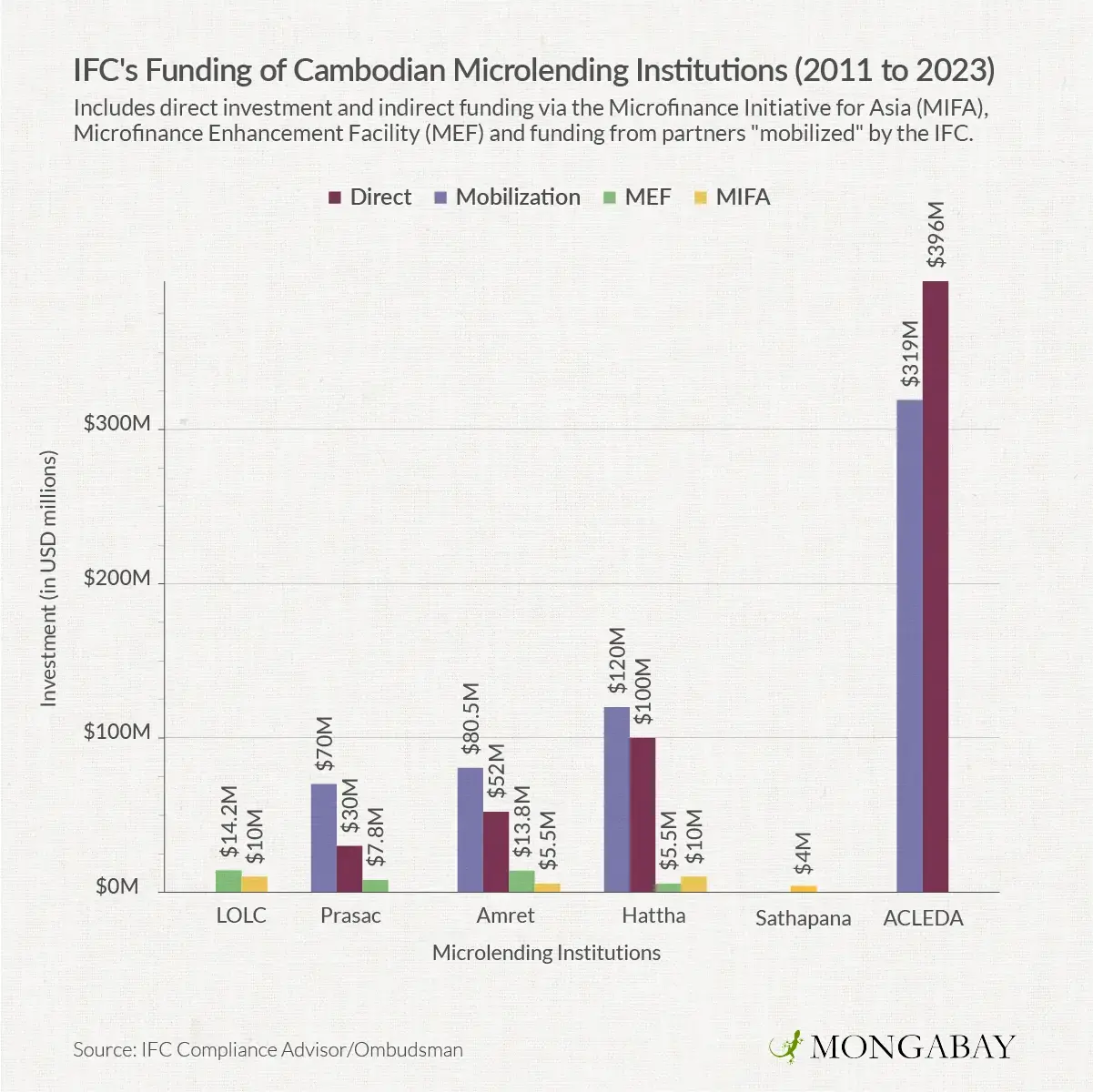

Since 2020, the World Bank Group has embarked on its $93 million third Land Allocation for Social and Economic Development (LASED III) project in Cambodia, focused in part on Indigenous communal land titling. Meanwhile, the organization’s private sector investment arm, the International Finance Corporation (IFC), has invested hundreds of millions directly and indirectly into the Cambodian microfinance sector since the 1990s.

These investments into six of Cambodia’s biggest microlenders are now in the crosshairs of the IFC’s internal watchdog, the Office of the Compliance Advisor/Ombudsman (CAO). The CAO is currently investigating whether the IFC violated its environmental and social governance standards, following a complaint supported by two local NGOs highlighting the impacts of over-indebtedness, including land loss in Indigenous communities.

“There’s a total contradiction there between, on the one hand, the World Bank trying to support communal land titling through LASED III and then the IFC giving loans to the microfinance industry, without considering how providing loans might work against the [Indigenous communal] land title,” says Ian Baird, a professor of geography at the University of Wisconsin-Madison, who has been working in northeast Cambodia since the 1990s and produced a 2023 study on the effect of microloans in Ta Heuy village’s titling process.

The World Bank Group and its LASED III implementing partner, Cambodia’s land ministry, didn’t respond to requests for comment.

Mongabay spoke with dozens of Indigenous villagers and representatives from five communities in Ratanakiri who cited microloans as the main reason for ending their ICLT applications. Indigenous Bunong leaders in several villages in neighboring Mondulkiri province noted a similar trend of microloans leading to divisions within their communities, undermining ongoing communal land titling efforts.

Staff at several Indigenous rights organizations also cited microloans as a significant threat to the future of securing Indigenous communal land rights in Cambodia.

Cambodia Microfinance Association (CMA) spokesperson Kaing Tongngy told Mongabay in an email that “everyone should have freedom to choose what is best for them, be it individual ownership or communal ownership.”

However, NGO representatives, Indigenous rights activists and researchers all noted that the present land rights framework and industry lending practices put communities in the position of having to choose individual titles at the expense of protecting culturally important lands and forests. Communities need both, they say.

“There needs to be efforts made to support those communities so they have access to credit and don’t feel they are losing out as a result of the communal land title,” Baird says.

Collateralizing community lands

Following an end to decades of conflict and instability, including the destruction of all property rights under the totalitarian Khmer Rouge regime between 1975 and 1979, Cambodia’s 2001 Land Law laid out the foundations of the Indigenous communal land title. It wasn’t until 2009 that the process for obtaining a communal land title was clarified, despite swaths of Indigenous lands already having been redistributed to companies through government-granted economic land concessions.

The ICLT process typically takes years and can cost more than $60,000, according to Nimol Van, Ratanakiri program manager for the Indigenous Community Support Organization. His NGO spearheads communal land titling in dozens of villages and has been assisting the World Bank’s LASED III project.

There are an estimated 24 Indigenous ethnic minority groups in Cambodia, comprising 2-3% of the country’s 16 million population, with more than 450 government-recognized Indigenous communities. But only 40 Indigenous communities have so far received communal land titles.

While communal land titles faltered due to authorities’ dragging their feet, Cambodia’s government promoted individual land titles nationwide via a 2012 land reform policy, prompting divisions among Indigenous communities.

And as Cambodia’s northeast opened up to global markets, communities shifted away from subsistence agriculture and forest products like resin and toward cash crops like cashew and rubber.

The ongoing transition has been increasingly fueled by microloans.

“Everyone needs loans to improve their development,” says Yun Lorang, secretary-coordinator of the Cambodia Indigenous Peoples Alliance, adding that land security is also essential for Indigenous communities. “We are in a globalized market system, we have to use machines, we need gasoline, fertilizer. They have no choice, if they don’t do that they cannot survive, it’s not like before.”

“Even if you get the communal land title, you still need access to money, when your children get sick, go to the hospital, for study, for everything you have to pay,” he adds. “So where can you get the money?”

Like many Cambodians, Indigenous communities have relied on microloans as a form of social welfare to cover health expenses or even to cover the costs of weddings, funerals and other important ritual ceremonies — except with 18% annual interest and no earnings on this investment, says Phasy Res, a researcher who studies microfinance in northeastern Cambodia.

In addition, many in Indigenous communities are particularly high-risk borrowers, lacking experience with financial institutions and fluency in Cambodia’s dominant language of Khmer.

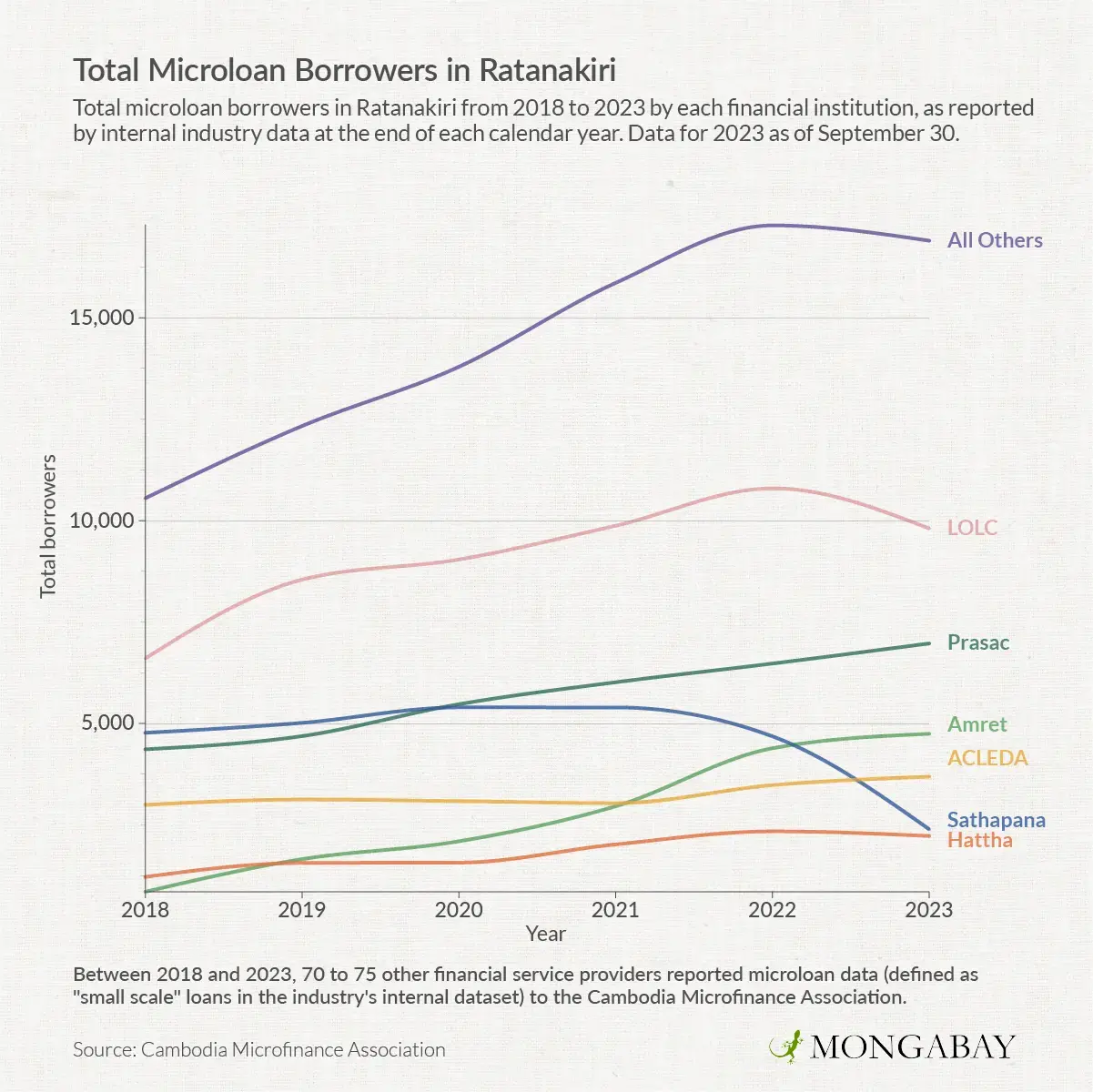

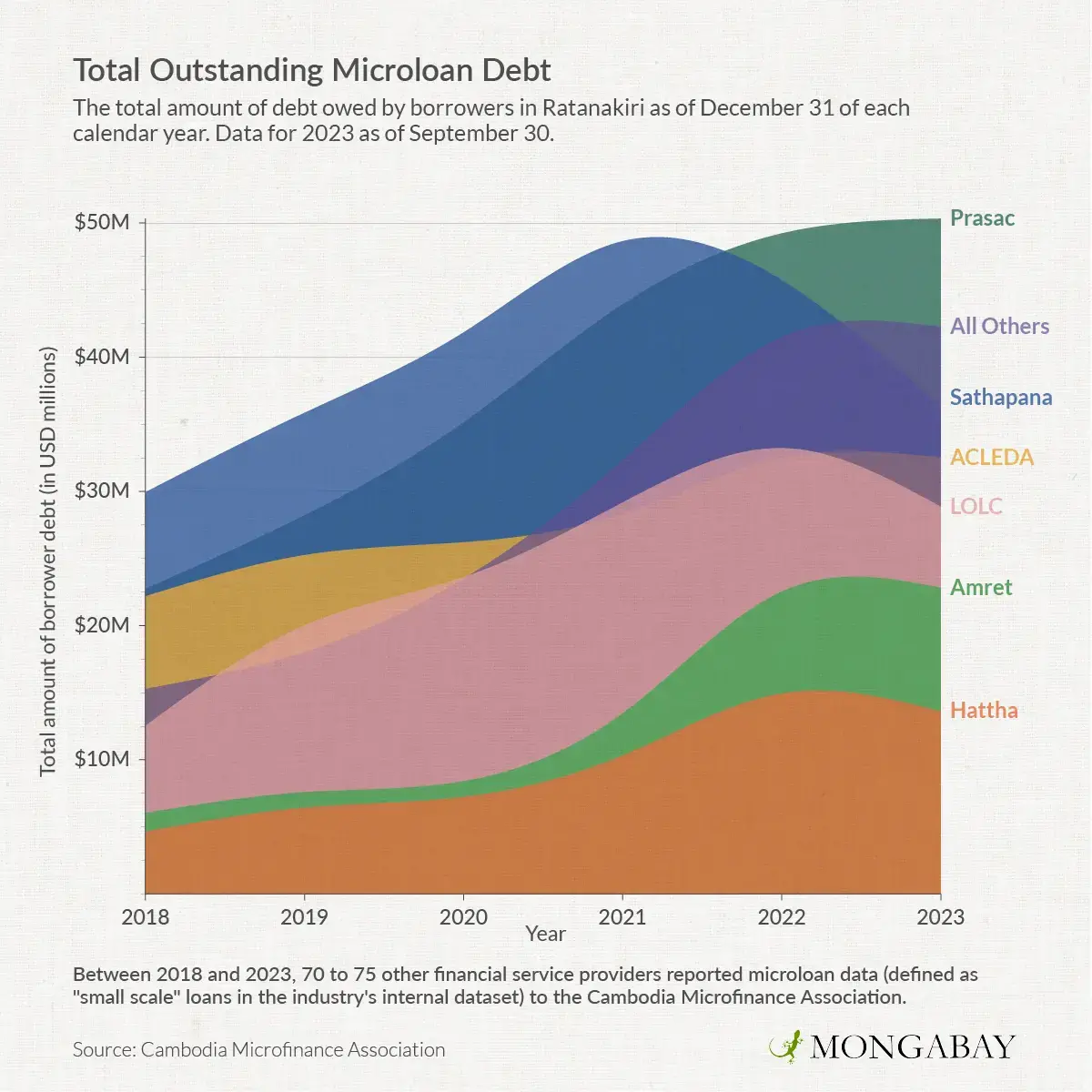

Internal industry data compiled by the CMA and obtained by Mongabay show that between 2018 and the third quarter of 2023, the amount of debt owed by Ratanakiri borrowers grew from about $111 million to more than $226 million, with the number of borrowers increasing from around 31,000 to more than 46,000.

Even so, only 13% of borrowers said they felt microloans had directly helped improve their lives, according to a 2024 quantitative study funded by the CMA. One in five borrowers in the study also said they were spending more than 70% of their monthly income to repay loans, exceeding an international benchmark for over-indebtedness. But in Ta Heuy, some people acknowledged that the community’s living standards had increased greatly, though this was also part of broader transformations in Cambodian society and Indigenous communities experiencing the effects of globalization.

“Before the loans, everyone just had a small house made from bamboo, they didn’t have a big house like now, or motorbikes; some even have cars, it is better than before,” says Prak Bunsoey, the chief of Teun commune, an administrative zone that includes Ta Heuy village.

Though some microlenders now offer uncollateralized “group” loans, where several borrowers assume responsibility for each other’s debt, the amount offered is capped, and many Indigenous borrowers told Mongabay they didn’t consider a group loan by itself sufficient to meet their needs or else were unaware group loans were an option.

Much more common across the industry is the use of individual land titles as collateral — which human rights organizations have pointed out leads to loans issued based on assets rather than income and gives the microlender significant psychological leverage over borrowers. One of the country’s biggest microlenders, KB Prasac Bank Plc., reported that 99.9% of its loans in 2022 were mortgaged with a land title. Another major microlender, ACLEDA, reported that about 95% of its loans were collateralized. Yet the industry does not operate this way in other countries with large microlending sectors, such as India, which since 2021 has defined microfinance as issuing “collateral free loans” to reduce risks for low-income borrowers.

As loan amounts increased in Cambodia, 60% of landowners in Teun commune sold land in the last five years, mostly to non-Indigenous “outsiders” and often to repay debts linked to microloans, according to Bunsoey.

Debt-driven land sales have been a well-documented consequence of the growth of Cambodia’s microfinance industry, underpinned by a 2022 study funded by the German government — one of the biggest boosters of microfinance in Cambodia — estimating over-indebtedness may have driven more than 167,000 land sales in the last five years.

Most of the more than 250 families in Ta Heuy village have microloans, according to deputy village chief Ba Bunthy, who says this has led to more forest clearance.

“You borrow money from the bank, then go to grab land,” Bunthy says. “You don’t have money to give back, so you go to a private lender and then give the land you took to the lender. The more land they can get, the more money they can get.”

Much of the Ta Heuy village’s 354-hectare (875-acre) reserve forest, intended to provide land security for future generations, has been cleared since around 2021, community leaders say. Farmers from the village and outside continue to chip away at the more than 100-hectare (250-acre) spirit forest, according to village chief Javieng Mie, and cashew trees are visible right up against the forest’s border.

Prak Songkhan, a resident of Ta Heuy village and former member of its ICLT committee, says he’s observed around a third of his community claiming and clearing previously forested land and is fearful of the long-term impacts.

“Without a collective land title, and continuing to take loans from the bank, we will lose everything,” Songkhan says. “At the end of the day, they will have to sell whatever they have to pay back, including their home, land, or belongings. The loss of culture and unity within the community will gradually happen.”

Increasing repayment struggles

In August, the IFC’s internal watchdog opened an investigation into its investments in six of Cambodia’s biggest microlenders, following allegations that they had for years violated the IFC’s strict policies, including those protecting Indigenous communities’ rights.

The six lenders — LOLC Cambodia, Prasac, Amret, Sathapana, ACLEDA and Hattha — represent around 75% of the Cambodian market; all offer loans in Indigenous villages that canceled their ICLT applications.

An IFC spokesperson noted that microfinance supports livelihoods but acknowledged “legitimate concerns” about the impacts of heavy debt on borrowers.

Naly Pilorge, outreach director of Cambodian human rights organization LICADHO, one of the NGOs that filed the IFC complaint, says investors must conduct independent audits in Indigenous communities in Cambodia as part of a “systematic debt relief programme” to alleviate “clear violations” of the IFC standards. But she says there remains “a continuation of the predatory business-as-usual practices.”

Internal industry data from 2023 suggest increasing over-indebtedness in Ratanakiri province. In December 2018, the CMA claimed that only 0.31% of the industry’s microloan portfolio in Ratanakiri was in arrears after 30 days. By Sept. 30, 2023, this number had risen to 6.7% (excluding ACLEDA, due to data irregularities), slightly above the nationwide rate of 6.5% that CMA reported for the microfinance sector.

In a spreadsheet of CMA data compiled from each microfinance company, under a column labeled “problems” in Ta Heuy village’s Koun Mom district, microlender Woori Bank reported “Loss of Agrculture [sic] Product, Multiple debt, Money lender and many MFI” — a comment it repeated for other districts in the province. No other microlender is listed as providing any other information, and Woori Bank, the local subsidiary of one of South Korea’s biggest banks, didn’t respond to requests for comment.

For some major lenders like Sathapana Bank, the amount of borrowers in Ratanakiri unable to make loan repayments appears to have drastically increased in the past five years, with non-performing loans after 30 days increasing from less than 1% in 2018 to more than 13% by mid-2023. Prasac, the largest microlender in the province, saw the percent of its loans in arrears after 30 days rise from 1.4% to 10.8% by the third quarter of 2023, in Ta Heuy village’s Koun Mom district.

Tongngy, the CMA spokesperson, acknowledged the rise in nonperforming loans in the province, which he attributed to the impact of “price fluctuation” and “climate change” on agriculture and a decline in tourism and the local economy tied in with global conflicts and the lingering impact of the COVID-19 pandemic.

Not every borrower is over-indebted, and many in Ratanakiri retain sizable land holdings even as they expressed stress over repayments. But it usually takes around five cycles of microloans before borrowers begin to run into trouble as loan amounts increase, says Res, the researcher.

And many Ta Heuy villagers’ experiences mirrored the well-documented negative impacts of microloans on several other of Ratanakiri’s Indigenous communities in a 2022 report by the NGOs LICADHO and Equitable Cambodia. The situation has been compounded by bad weather wrecking cashew harvests, which most people rely on to repay the principal of their loans.

Earlier this year, a young man in Ta Heuy committed suicide, one of several recent Indigenous suicides reportedly influenced by microloan debt in Ratanakiri. This left his pregnant widow, Lat Anthon, and her family under pressure from microlenders to sell the small farm representing their sole source of income.

Several highly indebted families in Ta Heuy who spoke with Mongabay say they had migrated, or planned to migrate, elsewhere in the country or to Thailand to earn enough to repay monthly microloan interest payments.

“This debt, it made us apart from each other, it felt like divorce,” says one villager, whose husband sold most of their land and then left to work at a far-away banana plantation to help them repay interest on more than $10,000 in debts to several microlenders. “For now, our life is getting worse and worse every day and whenever I have money from something, I just pay it to the bank and feel sick.”

Some people have lost much of their farmland, and psychological distress has gotten worse, villagers say. Private lenders charging more than 10% interest a month opportunistically compound the debt issues of desperate borrowers who engage in “debt juggling” between these private lenders and microlending firms.

“The bank always recommends you to get more loans when you don’t have money,” one indebted Ta Heuy villager says. “When we don’t have money to give back to the bank, they will bring you to the police station and recommend that you sell land.”

Of the six microlenders in the CAO’s investigation, only Amret and ACLEDA responded to Mongabay’s request for comment. An Amret spokesperson stated via email that Amret will “address issues as they arise” with Indigenous communities. ACLEDA CEO In Channy declined to comment, saying his bank “hasn’t have [sic] any loan portfolios in micro business anymore” — though industry data show that ACLEDA still offers “small scale” loans across Cambodia. The National Bank of Cambodia, the industry’s regulator, didn’t respond to requests for comment.

Limited alternatives and solutions to microloan debts

Fearing over-indebtedness, some Indigenous communities in Ratanakiri have participated in financial literacy classes to teach financial planning and management, though that means placing the onus of responsible financing on the borrower and not the lender.

There have also been grassroots attempts to promote savings groups and Indigenous community banks. In 2011, civil society groups sought to develop community banks for Indigenous villages across Ratanakiri, but the banks largely fizzled in part due to lack of capital and limited technical capacity.

In the ethnic Jarai community of Tang Se Malou, villagers have organized several savings groups to provide loans to each other and accrue interest as profit. The largest group, combining several dozen members, has around $9,000 with a borrowing limit of about $120 at a time.

“It is not enough, we still have to borrow from neighbors or microfinance,” says Tang Rolan, the leader of the youth savings group. Still, the savings group can help people deal with emergencies, such as medical crises.

Res, the researcher, says social welfare programs, not microloans, should cover health care and other basic needs of poor families.

Microlenders could take additional steps to mitigate harms to vulnerable borrowers, Res says. Industrywide, microlenders could allow for greater flexibility in repayment schedules to align with Indigenous communities’ actual income streams by making a lump sum payment at harvest time in lieu of the current monthly repayments. And microlenders should conduct regular assessments of how their loans are being used to ensure they aren’t undermining borrowers’ livelihood and land security, she adds.

Some limited interventions are taking shape: the industry is experimenting with offering crop insurance to reduce the risk that a bad harvest triggers over-indebtedness, as has been the case for farmers in Ta Heuy. But that policy is still in the pilot stage, the CMA’s Tongngy says.

For now, many Indigenous communities in Ratanakiri are still reliant on microloans to support their livelihoods, with little in the way of a safety net. In turn, the World Bank’s plans to help them obtain communal land titles appear to be falling short based on the dominant lending practices’ use of collateralized land titles.

In the ethnic Kreung community of Thuoy Ampil village, near the provincial capital, the village voted in 2022 to end its communal land title applications, despite meeting with the World Bank’s project team the previous year. The community still wanted protection for their cemetery, spirit and reserve forests, but not for their homes and farmlands because then they wouldn’t be able to take out loans or sell their land, says village chief assistant Baramey Chouy. Fertile red-soil farmland can sell for more than $10,000 per hectare, he notes, or about $4,000 per acre.

“I feel regret because if we don’t get the communal land title, everyone can sell land to people outside their village and their land is not protected, because everyone is short-thinking,” says Chouy, wearing a red shirt advertising Mohanokor, a large microlending company operating in the village.

In the more remote Ratanakiri village of Peng, an ethnic Jarai community also courted by the World Bank’s land titling team, village chief Romas Kyork says the community voted to stop pursuing their communal land title in May 2022 so they could continue taking out loans, often to repay existing debt.

A rubber company has already encroached on a chunk of the village’s spirit forest, and Kyork says he worries about the rest. He says that as long as he’s chief, he’ll bar his neighbors from selling land outside the community.

“That can make the community sell their land easily, if Khmer come from outside they buy and buy and buy, and small companies too,” Kyork says. “I don’t want my community to lose more land.”

His neighbor, 50-year-old Jin Pochom, is less concerned. He says he’s in a cycle of debt, taking thousands of dollars of microloans from one microlender to repay another, but adds it’s necessary for his farming. And besides, he says, he hopes to buy a new truck. Puffing on a large cigarette made from a leaf, he smiles.

“If we want to sell our land, it is up to us,” he says. “In the past, I could get whatever I wanted in the forest, but now all that is gone. In this era, it’s all about money. Even if you go to take a piss, you have to pay for it.”

View this story on Camboja News

View this story on Camboja News