Story

December 2, 2021

December 2, 2021

Covid-19′S Hidden Cost: Georgia Taxpayers Pay More for Public-Debt Financing

Country:

Project

The COVID Financial Crisis

In the first two months of the crisis, 14 percent of American workers filed for unemployment...

The human toll of COVID-19 — from lost lives to lost jobs — is front and center for families across Georgia still grappling with the pandemic.

But an analysis by The Atlanta Journal-Constitution reveals a hidden cost to Georgians since the start of the crisis — millions of dollars in added expenses for many cities, counties, school districts, hospitals and other entities to finance projects.

Call it a sort of COVID penalty.

Typically, governments issue municipal bonds to pay for large and expensive projects, borrowing the money from investors who buy the bonds. That’s how a judicial complex in Savannah, school projects in North Georgia and water lines in rural Monroe County near Macon were financed. But the borrowing costs are higher than would have been expected had the pandemic not happened, the AJC analysis shows, and will likely add up to hundreds of millions of dollars statewide.

That has made it more expensive for many Georgia governments to deliver vital services, the AJC found in analyzing 3,000 new bond issuances covering a three-year period around the pandemic. The debt expenses come as the costs for raw goods, labor and services also are soaring because of the lingering challenges of the pandemic.

The added costs come despite the early and largely successful federal intervention to prop up the bond market by buying the bonds. After bond pricing settled down in the summer of 2020 following the federal intervention, the AJC analysis shows costs started to climb again amid the second and third surges of the coronavirus in 2020.

The analysis also found that higher COVID-19 case rates in a jurisdiction during a given month preceded higher long-term costs for the bonds issued in that jurisdiction during the following month.

That raises questions about whether a more robust effort to control the virus could have lessened financial strains on taxpayers and governments, as well as saved more lives.

Not every local government has been impacted equally by this apparent COVID-19 penalty. A litany of variables contributes to how much local governments pay to borrow money in the municipal bond market.

Many issued debt or refinanced old bonds during the pandemic with favorable borrowing costs. The city of Sugar Hill saved nearly $4 million by refunding bonds issued before the pandemic, though the AJC analysis shows it is possible the Gwinnett County city could have saved more had the pandemic not happened. The city of Sandy Springs postponed a planned refinancing of bonds as the pandemic hit in early 2020, then after pausing to let the markets calm the city found lower interest rates that summer.

And even when the costs to local governments spiked, the burden to individual taxpayers is likely to be small. But the costs — to be paid via property and sales taxes and service fees in some instances — will add up across hundreds of governments and potentially many years of debt servicing.

The pattern of higher than expected borrowing costs also appears with municipal bonds for which taxpayers are not on the hook, such as bonds for some private student housing developments and non-profit hospital projects.

The AJC analysis examined the bonds and borrowing costs through the maturity of the debt. It’s possible jurisdictions could refinance their debts to more favorable rates in the future if market conditions allow.

One county’s experience

Monroe County, near Macon, didn’t have the luxury of waiting out the pandemic. In July 2020, it sold about $20 million in bonds to finance several projects, including to build dozens of miles of new water lines near the unincorporated community of Juliette.

The bond’s coupon rate, roughly equivalent to the interest rate on a mortgage or car loan, was 1.12% higher than the county’s average coupon before the pandemic. The AJC estimates Monroe County’s borrowing costs for its 2020 bonds will be about $2.5 million more over the life of the debt compared to the average rates the county received prior to the pandemic.

Juliette, with its quaint storefronts and famed Whistle Stop Café, enjoyed a starring turn in the 1991 film “Fried Green Tomatoes,” featuring Jessica Tandy and Kathy Bates. Like many rural stretches of Georgia, the area’s drinking water needs are largely served by wells drilled by individual property owners.

Juliette is also home to Plant Scherer, the nation’s largest coal-fired power plant. Dozens of residents near the Georgia Power facility sued the utility last year alleging contaminants from an unlined coal ash pond where power production waste is stored have seeped into their drinking water. The lawsuit alleges the waste has sickened nearby residents, which Georgia Power has denied.

Last year, the county accelerated plans to extend water service to Juliette residents.

County commissioners had hoped to refinance old bond debt from 2012 at the same time they issued the new bonds last year. But Monroe County Finance Director Lorri Lynn Robinson said officials opted against it because the borrowing costs were higher to refinance than if the county left the old debt unchanged.

“It made no sense to roll that into or pay it off with the new bond,” she said.

“When you build your budget, this is one of my expenses,” Robinson said of the amount of money Monroe County devotes annually to paying bond debt. “If I was able to save on my debt service amount, that money would go to something else.”

The 2020 bonds will be repaid through property taxes and the rates paid by water customers, including the new customers in Juliette.

“It’s tough to pinpoint the value of clean water,” said Brent Lackley, whose family sells souvenirs at FriedGreenTomatoes.com and from a shop across the street from the Whistle Stop Café. “You have to have it.”

Second, third virus waves push rates higher

A more disastrous impact to the municipal bond market loomed in March 2020, as states entered lockdown. Worried investors pulled money, causing borrowing costs to soar. Municipal bond yields — which can be thought of as real-time estimates of the current cost of borrowing — spiked, in many cases increasing over a 1,000%.

Conditions deteriorated to the point where Kent Hiteshew, deputy associate director of the Federal Reserve’s Division of Financial Stability, said that “state and local governments were effectively unable to borrow.”

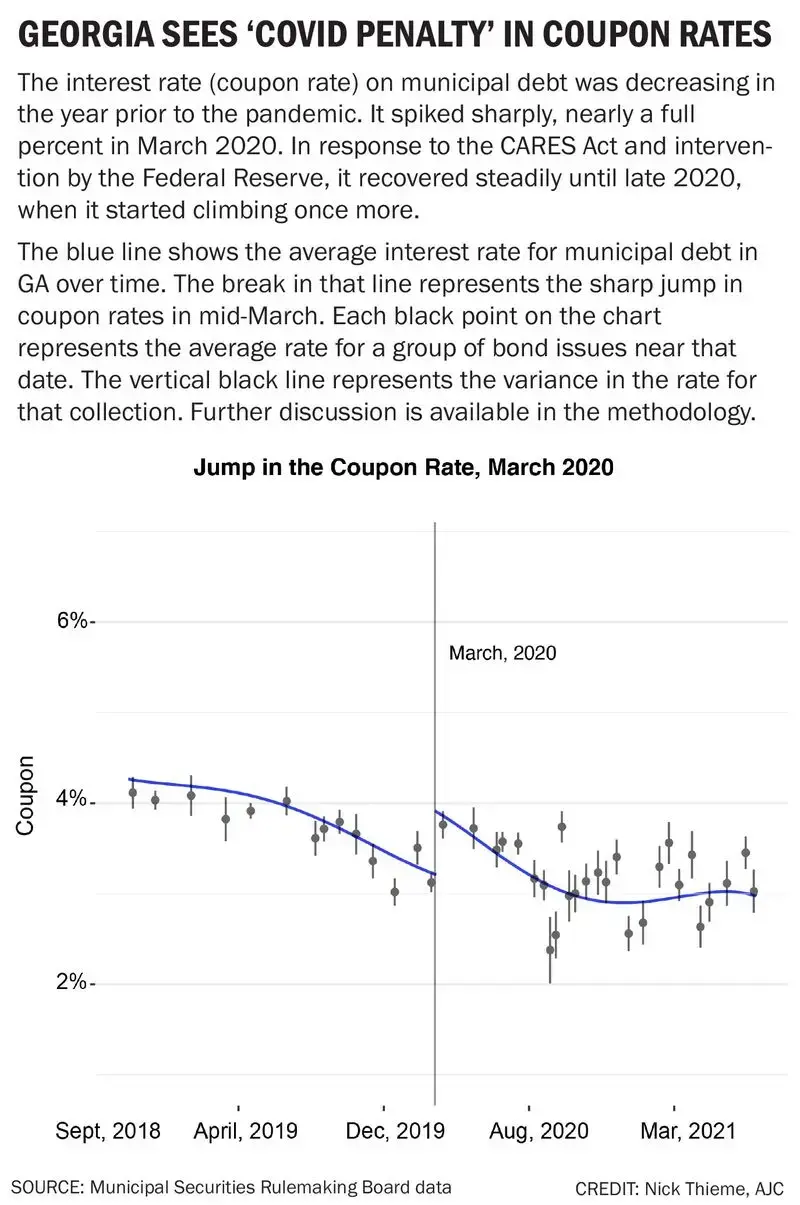

It was exactly at this point, in the third week of March 2020, that the interest rates of newly issued bonds in Georgia jumped from just about 3.1% to about 3.9%.

In the secondary market — where investors buy and sell municipal bond holdings — yields nearly doubled. The severity of the jump was strongly related to the number of COVID-19 cases near the municipality issuing the bond, the AJC found after controlling for the financial health and creditworthiness of issuers, specifics about the bonds and local and national economic trends.

The bond market substantially recovered in April 2020 after a $500 billion infusion from the Federal Reserve that was part of the $2.2 trillion in economic stimulus from the CARES Act of 2020.

“The scale of the fiscal stimulus was historic,” said Huixin Bi, a researcher at the Kansas City Federal Reserve Bank.

By mid-July, average interest rates had returned to their pre-pandemic levels. However, within a few months, the continuing pandemic led to worsening conditions for local governments in Georgia. Interest rates increased nearly to their pandemic high in fall 2020, as the second and third waves of COVID-19 spread.

“As the pandemic continues to drag on, these long-term credit concerns likely (increase),” said Bi.

The long-term issues with government funding were observed by financial ratings companies as well. Thomas Zemetis, associate director at S&P Global Ratings, said the S&P is now factoring COVID-19 into their credit ratings, watching both the spread of the virus and efforts to control it.

“As the viral conditions continue to change and the variants continue to introduce new risks, we also want to see what the control of the virus or the spread of the vaccine means for the economic condition.”

Higher costs for medical facility

The AJC analysis mostly examined government debt, but it also swept up borrowing and trading activity for bonds issued by government agencies on behalf of such institutions as non-profit health care companies.

These include about $220 million in bonds from 2017 used to complete construction of the Emory Proton Therapy Center, a cutting-edge cancer treatment facility near the Fox Theatre in Midtown Atlanta. The center relies on cancer specialists from Emory Healthcare, but it is owned and operated by a separate ownership group.

Financial reports show the Emory center saw a 30% reduction in average daily patients through the first nine months of 2020 compared to the center’s original projections.

In response, documents show the center instituted plans to reduce marketing and personnel costs and generate new revenue. The center’s amended budget for 2020 forecast a $36 million loss for that year after including long-term debt costs, and a $26.8 million reduction in revenue.

As a result, bond yields on the center’s debt grew from about 6% before the pandemic to a high of 12% in February, before settling about 10% as of late October.

The center’s 2022 budget also projects a nearly $36 million loss for the year.

The ownership group declined comment through an Emory spokeswoman.

How we got the story

To calculate the changing interest rates and how COVID affected them, the AJC data specialist Nick Thieme undertook a statistical analysis of municipal bond data obtained from the Municipal Securities Rulemaking Board (MSRB), the regulating body in charge of municipal bonds in the U.S. The MSRB provided real-time bond transaction data covering all bond trades in the U.S. between October 2019 and October 2021. Additionally, data on the roughly 3,000 new bond issuances between October 2018 and October 2021 were acquired. These data provided a complete record of all new bonds issued and characteristics of their issuance along with all bonds traded and characteristics of their trading.

The AJC also acquired metadata on issuers and issuances from S&P Global Services, a financial company tasked with maintaining bond records. These data included the jurisdiction covered by a bond, the economic sector a bond pertains to, and financial characteristics of the bond. Demographic data on covered jurisdictions was obtained from the U.S. Census Bureau. Data on new COVID cases over time comes from the AJC’s database of COVID cases. Data on economic conditions over time comes from the Federal Reserve Economic Database (FRED).

Following strategies developed by public and private sector economic analysts, the AJC cleaned the data, and linked the datasets together to create a usable dataset of new bond issuances, metadata about the issuance, economic and demographic data for the region the bond pertains to, and COVID cases in that same area. To determine whether bond coupons were higher before or after March 2020, the AJC used a so-called regression discontinuity design model. These models are considered the best post-treatment methods for causal inference.

Lastly, to estimate the size of the effect of COVID-19 on bond coupons, the AJC built a series of statistical models, increasing in complexity from a simple linear model, to general additive models (GAM), to mixed-effects GAMs, to mixed-effects GAMs with a large degree of freedom. These models were then used to estimate the effect of COVID, and all showed almost total agreement.

This methodology was vetted by Michael Lavine, professor of statistics at the University of Massachusetts Amherst.

A full white paper with the data, exploratory data analysis, and model diagnostics is available here.